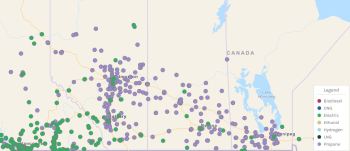

March 2018 - Court Ordered Sales

March 2018 - Maple Ridge - detached

March 2018 - Burnaby - attached

March 2018 - Sunshine coast - attached

March 2018 - Richmond - attached

March 2018 - West Vancouver - detached

March 2018 - Vancouver - detached

March 2018 - Richmond - detached

this months trends again are more detached then attached listings.. most detached foreclosures this month are in prime areas ( Vancouver, West Van & Richmond) interesting trend to keep an eye on...

7 Top Tax Refund Dos and Don’ts: It’s Your Money, Don’t Blow It!

What to Do With Your Tax Refund:1. Pay Off Any High-Interest Debt First

It doesn’t sound sexy, but if you can knock out some debt (often credit card debt) that’s costing you money each month, you can take a huge positive step financially. There are different approaches like paying off the highest interest or paying off the biggest amount first (which can sometimes mentally be a big motivator), so look at various options for paying off credit card debt to make it work best for you.

2. Stash Money Away for an Emergency Fund

Only 39% of Americans say they’d be able to cover a $1000 emergency expense with savings, according to a 2018 Bankrate survey. If you’re in the majority who doesn’t have that savings stashed away, it’s a good idea to save money for a rainy day in case you need it. An emergency fund will keep you from having to charge emergency costs on higher interest credit cards or having to get creative to pay for something that pops up.

Continue Article Here...

The Top 5 Real Estate Calculations Every Investor Should Memorize

Despite what many of us math-allergic folk would prefer, real estate does involve some math. Luckily, most of the formulas are simple and straight-forward. In fact, if you can master the calculations below, you should be just fine.

1. CAP RATE

Net Operating Income / Total Price of Property

This calculation is mostly used for valuing apartment complexes and larger commercial buildings. It can be used for houses and small multifamily too, but operating expenses are erratic with houses (because you don’t know how often and how bad your turnovers will be).

You want to have a cap rate that is at least as good, preferably better, than comparable buildings in the area. I almost always want to be at an 8 cap rate or better, although in some areas like Vancouver or Toronto, that’s not really possible. And always be sure to use real numbers or your own estimates when calculating this. Do not simply use what’s on the seller-provided pro forma.

2. RENT / COST

Monthly Rent / Total Price of Property

This is a great calculation for houses and sometimes small multifamily apartments. That being said, it should only be used when comparing the rental value of like properties. Do not compare the rent/cost of a property in a war zone to that in a gated community. A roof costs the same, square foot for square foot, in both areas. And vacancy and delinquency will be higher in a bad area, so rent/cost won’t tell you what your actual cash flow will be. The the old 2% rule can lead investors astray, and they shouldn’t use it. But when comparing like properties in similar areas, rent/cost is a very helpful tool.

For cash flow properties, you definitely want to be above 1%. We usually aim for around 1.5%, depending on the area. And yes, I would recommend having a target rent/cost percentage for any given area.

3. GROSS YIELD

Annual Rent / Total Price of Property

This is basically the same calculation as above but flipped around. It’s used more often when valuing large portfolios from what I’ve seen, but overall, it serves the same purpose as rent/cost.

4. DEBT SERVICE RATIO

Net Operating Income / Debt Service

This is the most important number that banks look at and is critical for getting financing. Generally, a bank will look at both the property’s debt service ratio and your “global” debt service ratio (i.e. the debt service ratio of your entire company or portfolio).

Anything under 1.0 means that you will lose money each month. Banks don’t like that (and you shouldn’t either). Generally, banks will want to see a 1.2 ratio or higher. In that way, you have a little cushion to afford the payments in case things get worse.

5. CASH ON CASH

Cash Flow / Cash In Deal

In the end, this is the most important number. It tells you what kind of return you are getting on your money.

This is a critical calculation not only when it comes to valuing a property, but also when it comes to evaluating what kind of debt or equity structure to use when purchasing it.

The math isn’t that bad. No rocket science here luckily. Instead, there are just a few handy calculations and rules to evaluate properties before purchase and analyze their performance afterward. Memorize these, and you should be fine.

|