December away in Mexico

A Happy New year to you. This is my first newsletter for a few months. It was a very busy 2025 with work and a few other things. This year, I hope to become better at delegating my tasks and managing time so as to leave room for very important things like sending out my newsletter!

We spent the latter half of December in Cancun Mexico. Being a history and archeology enthusiast, this region has been on my bucket list for a while mainly due to a fascination over the Mayan ruins. Also significantly, this was precisely the spot where the asteroid that exterminated the dinosaurs landed from space. Lest I forget, there is sunny weather, white sand, crystal clear ocean etc as well lol.

It was unbelievable to see the level of sophistication that went into construction of the Mayan complex 3000 years ago which included the pyramid shown in the picture. The kids had fun with the acoustics - when you shout, at the pyramid, you hear a powerful "delayed" echo of your voice.

The asteroid impact also left a huge footprint on the geology of the area. It caused the rocks undergroud to have holes like swiss cheese causing all the rivers in the area flow underground. Surface water is barely visible, yet the whole Yucutan peninsula is covered by lush vegetation. A big thank you to our Mayan tour guide for all the education.

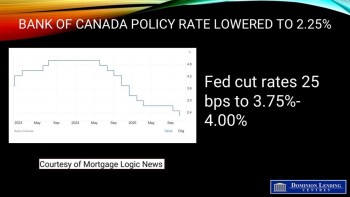

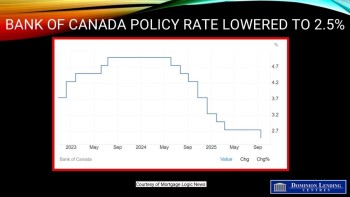

Do You Have A Mortgage Rate Closer to 5%?

I've worked the numbers for many of my past clients and their referrals and we have found some good opportunities to save money on their mortgage.

Many have taken the advice and have gone through a successful redo of their mortgage. For many, a lower rate and the penalty to get their did not make sense so we have left things alone. For many the savings have been worth the effort

If I haven't contacted you yet, or you want to revisit your numbers, or know someone that could use a check in, please let me know.

If You Passed Away Tomorrow?

If you passed away tomorrow, would your family know where to find anything?

If the answer is no, this article is for you. I’m talking about something most people avoid, but every family needs.

It’s called an “In Case of Death” folder on your computer. And this will be one of the most valuable things you ever leave behind for your loved ones. When someone passes away, families are left scrambling for documents, passwords, accounts, and instructions. A simple folder can prevent months of stress, confusion, and even financial loss.

So here’s exactly what should be inside. The first sub-folder should contain your personal identity documents. These are often the hardest things for families to find. Include your birth certificate, your marriage certificate, your driver’s license, and any provincial ID. Anything that confirms who you are and who should handle your affairs.

The second folder should contain your legal and estate documents. This includes your last registered will, your power of attorney, your health care directives, and your succession certificates. If you have minors, this is also where you keep all legal guardianship documents. These documents decide everything if something happens, so keep them easy to find.

The third folder should contain all your financial assets. Add your bank account details, investment information, and safety deposit box location and key details. Include all loan documents and all insurance policies as well. Your executor can’t manage what they can’t find.

The fourth folder should contain everything related to real estate you own, and any business documents if you own a company. Add your property agreements, mortgage agreements, rental agreements, and business succession plans. This makes transferring or managing your assets far simpler. The fifth folder should contain your digital assets. This includes your domain names, email addresses, user IDs, and passwords. Ideally, use a password manager that automatically sends access to your emergency contact if you’re inactive for 30 to 60 days.

Finally, make sure a trusted family member or lawyer knows this folder exists and can access it. Setting this up takes less than an hour, but it can save your family from months of hardship.

|