Tougher Mortgage Rules Coming Jan 1, 2018

As of January 1, 2018, there are new rules requiring all new mortgages to qualify at the Bank of Canada (BoC) benchmark rate, or 2% higher than the contract rate.

The contract rate is the rate you are quoted on the mortgage you are qualifying for.

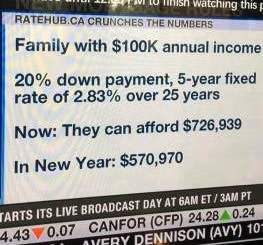

What does this mean? Your going to lose around 20% of your purchasing power as of January 1.

Well that isn't completely the case, because some lenders have already started the stress test, and at least one other is starting it on December 15.

Is there a way around this? No. (Well, maybe...)

Are there other options?

Technically, yes. Provincially regulated lenders such as credit unions do not have to follow these rules. It only applies to federally regulated lenders such as big banks or monoline lenders (companies that only do mortgages).

However, it's possible that these credit unions will implement the same rules.

What can you do?

If you want to refinance or structure line of credits, do it NOW!! If you were planning to buy in 2018, buy NOW.

What is the long run ramification of this?

More people will require mortgage planning to qualify, and that's why you want to work with a mortgage agent like me.

Maybe you don't want me to tell you this now, but 10 years ago, you were able to buy a property in Canada with 0% down, self-employed stated income mortgages. If you had a pulse, you qualified! (I am sort-of kidding.)

Today, they need detailed financials to qualify with minimal exceptions allowed.

Five years from now, they will require your DNA sequenced! (Just kidding... or am I?)

Curious what to do?

Call me @ 416.707.1020 or message me and we can have a quick chat.

|