Should You Buy Disability Insurance if You Are Incorporated?

If you're incorporated, securing private disability insurance is essential. Relying solely on government disability benefits, such as the Canada Pension Plan (CPP), will not provide adequate income replacement if you're unable to work.

As of 2024, the maximum monthly CPP disability benefit is $1,606.78, totalling about $19,281.36 annually. For someone earning $150,000, $250,000, $500,000, or even $1 million per year, this represents a drastic reduction in income.

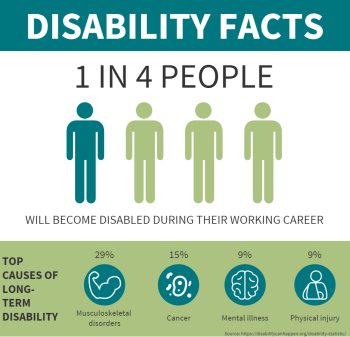

Here are the 10 most common reasons people become disabled:

Musculoskeletal disorders – Back pain, arthritis, and other joint or muscle issues.

Cancer – Various types, often requiring long-term recovery or treatment.

Injuries – From accidents, including fractures, sprains, or severe trauma.

Mental health disorders – Depression, anxiety, and stress-related conditions.

Cardiovascular conditions – Heart disease, stroke, or other heart-related issues.

Nervous system disorders – Conditions like multiple sclerosis, Parkinson’s disease, or epilepsy.

Diabetes complications – Vision loss, amputations, or other severe effects.

Respiratory disorders – Chronic conditions like asthma, COPD, or lung disease.

Pregnancy-related issues – Severe complications requiring extended leave.

Digestive disorders – Chronic illnesses such as Crohn’s disease or ulcerative colitis.

The trick with disability insurance is to purchase high-end private coverage. Only two companies provide this product: RBC and Canada Life.

Message back if you'd like to run some numbers.

|