What's Going on with Rates?

Fixed mortgage rates have increased between .50% to .60% over the last couple of weeks. This is largely due to the Bank of Canada ending quantitative easing (QE). QE was a stimulus program that was introduced at the start of the pandemic to pump money into the economy. What it also did was artificially lower the bond prices and by extension the fixed mortgage rates. Taking away the stimulus raised the price of bonds and immediately increased the fixed mortgage rates. It became more expensive for lenders.

Depending on who you talk to, by eliminating Quantitative Easing and moving up the timetable for future policy rate hikes, the Bank of Canada was either reacting to the impending doom of increased inflation, or the risk of inflation is way overblown, and the Bank of Canada acted to calm the fears of the market.

With people returning to work, and the economy doing well, we run the risk of inflation getting out of control. On the other hand, we're not nearly out of the COVID woods, and a full recovery is still a ways out and any future policy changes should be delayed.

For variable rates, Scotiabank announced that it expects the Bank of Canada to deliver eight quarter-point hikes (totaling 200 basis points, or 2%) by the end of 2023. Housing analyst Ben Rabidoux, says the fear of rate hikes is overblown, and that eight hikes in the next two years is close to a “pipe dream.” To keep things in perspective, the other big banks expect anywhere between one and three Bank of Canada rate hikes by the end of 2023.

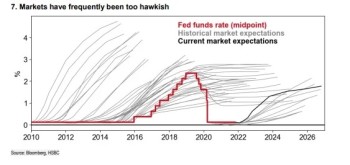

Take a look at the above graph. The light grey lines shows the various predictions and the red line shows the actual increases. Coming out of the 2009 recession, predictions were much more aggressive than what actually happened. I expect that we will see a very similar outcome, considering that Canadians are extremely risk-sensitive.

An increase by the Bank of Canada's policy rate would directly impact the variable rate mortgage rates and by extension the monthly payment. Every 0.25% increase would be the equivalent of $13/month for every $100K in mortgage outstanding. A $500K mortgage would increase by $65/month.

My crystal ball is still cloudy, but if history repeats, an aggressive hike in the Bank's policy rate seems very unlikely. Fixed rates on the other hand seem to be settling into this range. Any future economic recovery news will likely push the fixed rates a bit higher.

Reach out to me to discuss your specific situation and if locking into a fixed rate is the right move.

Book of the Month - A World Ablaze

Every month I will be featuring a book I've read. This month's feature is 'A World Ablaze' by Craig Harline.

A Ken's Korner reader, Maria M, recommended this book to me. I thought it might be kinda boring but found it to be a very interesting account of the rise of Martin Luther and the Birth of the Reformation.

Set in the 16th century, the author, historian Craig Harline, does a great job of following Luther throughout his years beginning in 1517 when he was a monk/friar and going on to his death in 1546.

|