Foreclosures

Sept 2025 Burnaby Detached

Sept 2025 Chilliwack Attached

Sept 2025 Abbotsford Attached

Sept 2025 Chilliwack Detached

Sept 2025 Langley Detached

Sept 2025 Burnaby Attached

Sept 2025 Abbotsford Detached

Sept 2025 Maple Ridge Attached

Sept 2025 Langley Attached

Sept 2025 Maple Ridge Pitt Meadows Detached

Sept 2025 South Surrey White Rock Attached

Sept 2025 North Van Attached

Sept 2025 New West Attached

Sept 2025 Richmond Detached

Sept 2025 Mission Detached

Sept 2025 Tricities Detached

Sept 2025 Tricities Attached

Sept 2025 South Surrey White Rock Detached

Sept 2025 Surrey Attached

Sept 2025 Richmond Attached

Sept 2025 West Vancouver Detached

Sept 2025 West Vancouver Attached

Sept 2025 Vancouver Detached

Sept 2025 Vancouver Attached

Sept 2025 Surrey Detached

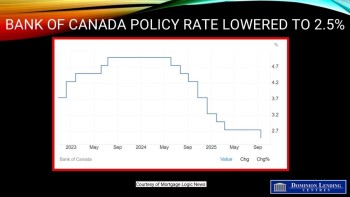

Bank of Canada Lowers Policy Rate to 2.5%

By Dr. Sherry Cooper - Chief Economist, Dominion Lending Centres

The Bank of Canada lowered the overnight policy rate (for Variable Rate mortgages) by 25 bps to 2.5% as was widely expected. Following better-than-expected inflation report, the Bank believes that underlying inflation was 2.5% year-over-year.

Through the recent period of tariff turmoil, the Governing Council has closely monitored the risks and uncertainties facing the Canadian economy. Three developments triggered the Bank's rate cut. Canada's labour market softened further. Upward pressure on underlying inflation has diminished, and there is less upside to risk to future inflation with the removal of most retaliatory tariffs by Canada.

Considerable uncertainty remains. However, with a weaker economy and less upside risk to inflation, the Governing Council deemed that a reduction in the policy rate was appropriate to better balance the risks going forward.

"The Bank will continue to assess the risks, look over a shorter horizon than usual, and be ready to respond to new information."

Continue reading here...

Fixed vs. Variable Mortgages: When Certainty Weighs Against Flexibility What’s Changing in the Market?

Tightening deals on both ends: While some of the most competitive fixed mortgage rates—like 5‑year terms edging under 4%—are fading, discounts on variable-rate mortgages are being trimmed too. Lenders such as CIBC and Scotiabank have offset less off their prime rate by about 10–15 basis points.Canada Mortgage News

Why the pullback? Lenders aren’t simply responding to swap or hedging pressures. Increased market volatility has prompted a cautious stance. Banks are trimming variable discounts in anticipation of possible abrupt rate moves, preserving their financial risk buffer.Canada Mortgage News

What’s Still in Your Favor?

Variable rates holding room to fall: Despite diminished discounts, variable mortgage rates could still offer long-term savings, especially if the Bank of Canada reduces the policy rate further.Canada Mortgage News

Bond yields setting pace for fixed rates: Fixed rates closely track bond yields, particularly the 5-year Government of Canada yield, which itself is influenced by U.S. Treasury movement. If global investor sentiment shifts, fixed rates could react quickly.Canada Mortgage News+1

Lending Strategy: Match Your Mortgage Type to Your Personal Profile Borrower TypeSuggested ApproachFlexible – Rate-WatchersVariable Rate: If you can absorb potential fluctuations and benefit from future cuts, variable is likely cheaper over time.Canada Mortgage News+1Cautious – Stability SeekersFixed Rate (3 or 5 years): Offers peace of mind with predictable payments. A 3‑year fixed can be particularly attractive in the current climate.Canada Mortgage News+2Canada Mortgage News+2Balance-OrientedHybrid Mortgage or Split Financing: This lets clients blend stability with optional upside—though some experts argue it may dilute the clarity of your financial bet.Canada Mortgage News Mortgage Penalties: Fix or Variable?

Fixed-rate mortgages usually come with steep penalties upon early break (Interest Rate Differential or IRD), which can bite hard if you refinance mid-term.

Variable-rate mortgages, on the other hand, often have much smaller penalties—typically only three months’ interest—offering much greater flexibility.Canada Mortgage NewsReddit

How to Translate This Into Client Education

Explain the Current Market Forces:

Fixed rates are rising with bond yields.

Variable discounts are narrowing, shrinking savings—but not eliminating them.

Clarify the “Why”—and the Downside:

Lenders are guarding against unpredictable shocks.

Variable still holds upside if the Bank of Canada cuts rates further.

Help Clients Align Their Choice with Their Comfort Level:

Risk-tolerant? Show the long-term benefit scenario for variable.

Preference for consistency? Show the predictability fixeds bring.

Open to compromise? Hybrid structures—but with caveats.

Always Factor in Penalties:

Emphasize how variable mortgages can offer flexibility, especially valuable if life circumstances change.

In Summary for Clients:

Fixed mortgages offer stability—but often come at a higher cost and stricter exit penalties.

Variable mortgages, though seeing eroding discounts, still pose a cost-saving opportunity—especially if interest rates decline.

Selecting the best path depends on individual financial goals, risk appetite, and personal life plans.

Let me know if you'd like to tailor this messaging for different borrower profiles or include real-world examples to enhance clarity!

|